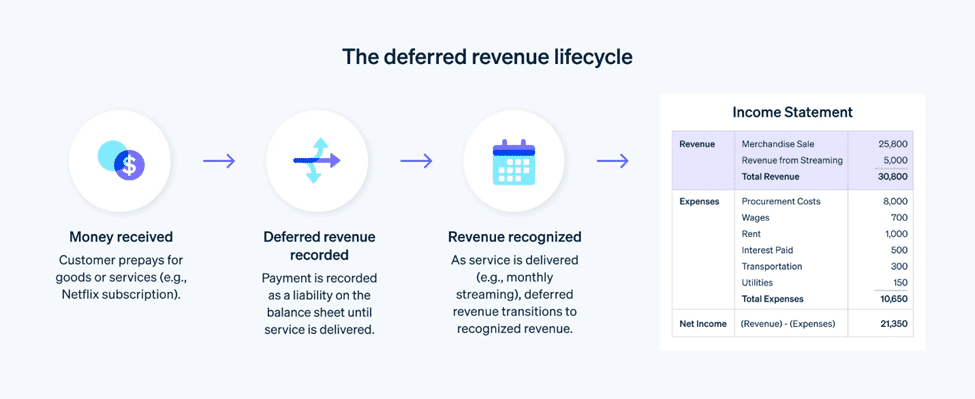

Deferred revenue is money received before delivering goods or services—commonly seen in prepaid service agreements and milestone-based project billing.

It’s a liability, not an asset, because it represents an obligation to your customer until services are performed.

Accurate journal entries—such as debiting Cash and crediting Deferred Revenue—are critical for compliance, clarity, and solid cash flow tracking.

Revenue recognition should happen as work is completed—monthly for service contracts or incrementally in project-based billing.

Tools like QuickBooks and Total Office Manager support proper setup using the correct account types (Other Liability for deferred revenue; Income for recognized revenue).

Project-based contractors should treat milestone payments as deferred until related work is done, using job costing to track progress and revenue recognition.

I get a lot of questions from my consulting clients—things like: What is deferred revenue? How do you make a deferred revenue journal entry? Is it an asset? Is it a liability? And many more.

Because of this, I decided to write an article on the subject of deferred revenue to hopefully answer all of these questions in one place. I have also included an example of how to make an adjusting journal entry that can be used in QuickBooks, Total Office Manager, and other accounting ERP (Enterprise Resource Planning) software.

What is Deferred Revenue?

Deferred revenue, also known as unearned revenue, is an important accounting concept, especially for HVAC and plumbing companies that often receive payments in advance for services. But what exactly is deferred revenue? In simple terms, deferred revenue represents money received by a company for goods or services that have yet to be delivered or performed.

Deferred Revenue Meaning

Think of deferred revenue as a promise—a promise to your customers that you will provide them with the services they’ve paid for. It’s like getting a subscription to your favorite magazine; you pay upfront, but the magazines arrive over time. Similarly, when your HVAC or plumbing company receives payment for a service contract upfront, that payment becomes deferred revenue until the service is actually provided.

Yes, deferred revenue is a liability. Why? Because it represents an obligation to provide goods or services in the future. Until you fulfill this obligation, you owe your customers the value they paid for in advance.

No, deferred revenue is not an asset. An asset represents something you own that has value, such as cash or equipment (e.g., accounts receivable or inventory). Deferred revenue, on the other hand, is an obligation—a promise to perform services or deliver goods in the future. Therefore, it is recorded as a liability on your balance sheet.

Deferred Revenue on Balance Sheet

Image by stripe.com

Deferred revenue appears on the balance sheet under the liabilities section. It’s important to note that as you provide the services or deliver the goods, deferred revenue is gradually recognized as actual revenue. This transition moves the amount from the liabilities section to the revenue section on the income statement.

How to Record Deferred Revenue in Accounting Software

Recording deferred revenue properly ensures your financial statements accurately reflect your business’s financial health. Let’s break it down with an example using debits and credits:

Example Adjusting Journal Entry

Imagine your HVAC contracting or plumbing company receives a $12,000 payment in advance for a one-year service contract. You need to record this payment as deferred revenue initially. In QuickBooks and Total Office Manager, select the account type of ‘Other Liability’ for your ‘Deferred Revenue’ account in your chart of accounts.

Each month, as you provide the service, you recognize part of the deferred revenue as actual revenue. For instance, after the first month, you would recognize $1,000 as revenue (since $12,000 divided by 12 months equals $1,000 per month):

Repeat this process each month until the entire $12,000 is recognized as revenue.

In QuickBooks and Total Office Manager, select the account type of ‘Income’ for ‘Service Revenue’.

How to Setup Deferred Revenue in QuickBooks®

In QuickBooks and Total Office Manager® from Aptora, select the account type of ‘Other Liability’ for your ‘Deferred Revenue’ account in your chart of accounts.

Deferred Revenue and Project-Based Billing

In construction and field service industries, many jobs are billed in stages or with milestone payments. That means a single project might generate multiple deferred revenue entries over its life cycle.

For example, if a plumbing contractor is paid 30% upfront, 40% at midpoint, and 30% upon completion, each of those payments should be treated as deferred revenue until the corresponding work is completed. This segmented recognition allows for cleaner financials and more precise job costing.

Set up clear policies in your accounting system to allocate each payment appropriately. Use job costing reports to track how much work has been completed and match revenue recognition accordingly. This alignment supports accurate profitability analysis and stronger forecasting.

Why Deferred Revenue Matters in the Field

Deferred revenue is more than just an accounting formality—it reflects your company’s accountability. When your business collects payments upfront, especially for long-term service agreements, those funds aren’t truly yours until the work is done. Mismanaging deferred revenue can cause major issues, from inaccurate financials to compliance problems.

For contracting businesses, properly managing deferred revenue ensures you never get ahead of your actual earned income. This matters especially when you’re using those upfront payments to pay expenses before earning the revenue. It’s easy to think you have more cash than you really do, which is why treating deferred revenue as a liability is so important.

Managing deferred revenue appropriately helps ensure that your financial statements are accurate and reflect the true financial health of your business. By properly recording and recognizing deferred revenue, you can avoid overstating your income and ensure that you meet your financial obligations to your customers.

Conclusion

Deferred revenue might sound like a complicated accounting term, but with a clear understanding and the right tools, it’s completely manageable. It’s a liability because it represents services or goods your business still owes to your customers, and treating it that way keeps your financials honest.

From simple monthly service contracts to complex, milestone-driven projects, understanding how to record, recognize, and report deferred revenue helps you avoid overstating income and maintain financial stability.

So, whether you’re using QuickBooks, Aptora 360, or another ERP system, follow these best practices and stay ahead of your accounting obligations. Your future self—and your financial statements—will thank you.

Quick Recap on Deferred Revenue

Deferred Revenue Meaning: Money received in advance for services or goods yet to be delivered.

Is Deferred Revenue a Liability?: Yes—it’s money you haven’t earned yet.

Is Deferred Revenue an Asset?: No—it’s not owned value; it’s an obligation.

How to Record Deferred Revenue: Debit Cash, Credit Deferred Revenue; recognize revenue as work is performed.

Why It’s a Liability: Because it’s tied to future work you’re committed to doing.

Project-Based Billing: Treat partial payments as deferred revenue until work is completed.

Why It Matters: Helps you avoid cash flow illusions and keeps your financial reports accurate.

Now, you’re ready to tackle deferred revenue with confidence! Happy accounting!

Frequently Asked Questions

Q: Why is Deferred Revenue a Liability?

A: Deferred revenue is considered a liability because it represents a future obligation. When customers pay you in advance, you owe them the service or product they paid for. Until you fulfill this obligation, the payment is a liability on your balance sheet.

Q: What Type of Account is Deferred Revenue?

A: Deferred revenue is a liability account. It’s listed under current liabilities if the service or product is expected to be delivered within a year. If the delivery is expected to take longer than a year, it can be classified as a long-term liability.

In QuickBooks and Total Office Manager, select the account type of ‘Other Liability’.

Q: What Are Deferred Revenues?

Q: Deferred revenues are simply amounts received by a business in advance of delivering goods or services. These amounts are recorded as liabilities until the corresponding goods or services are provided, at which point they are recognized as revenue.

Q: Deferred Revenue Definition in Accounting

A: In accounting, deferred revenue is defined as revenue that a company has received but has not yet earned. This revenue is recorded as a liability on the balance sheet because it represents an obligation to deliver goods or services in the future.

Share:

Facebook

Twitter

Pinterest

LinkedIn

James R. Leichter

James R. Leichter, renowned HVAC business consultant, author, and public speaker, is dedicated to empowering HVAC businesses with innovative strategies and insights. Leichter, affectionately known as 'Mr. HVAC,' brings over 27 years of industry expertise and a passion for practical solutions, assisting HVAC businesses to streamline operations and maximize profits. Discover transformative guidance at MrHVAC.com.

Quick Answer The purchase order (PO) process is the step-by-step workflow businesses use to control purchasing, approve spending, document vendor agreements, verify deliveries, and pay