Over my many years in the field service industry, I’ve learned that the way you look at your numbers can really make or break you and managing the finances of a retail business is nothing short of a balancing act. This is because you’re not just ringing up sales; you’re also tracking inventory, managing vendors, and trying to forecast for next season, all while trying to keep a close eye on your bottom line.

For amateur business owners and new accountants, stepping into the world of retail accounting can feel really overwhelming, but it doesn’t have to. Consider this your playbook. In this guide, I will provide you with an exact framework you can use to cut through the financial noise and chaos, build good financial routine, and master the innerworkings of your retail accounting.

Key Takeaways

Retail accounting tracks every dollar flowing in and out of your business, from daily sales to payroll and inventory.

Inventory valuation directly impacts profitability because it determines your Cost of Goods Sold and net income.

Choosing the right accounting method matters whether you use RIM, FIFO, LIFO, or weighted average cost.

Cash flow management is critical to survival since a business can be profitable on paper and still run out of cash.

Accurate financial statements guide decisions by revealing what you own, what you owe, and whether you’re truly making money.

Consistent expense categorization improves clarity and turns raw transactions into actionable insights.

Modern accounting software increases visibility and efficiency by integrating sales, inventory, and financial reporting in real time.

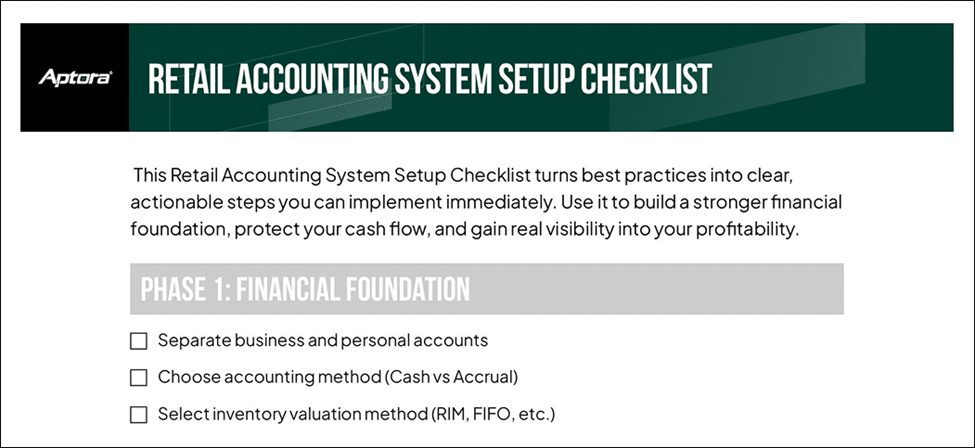

📥 Free Download:If you’re serious about strengthening your retail finances, don’t leave it to memory or good intentions. Grab our FREE Retail Accounting System Setup Checklist and follow a clear, step-by-step framework to tighten your bookkeeping, inventory, and cash flow management today!

Let’s begin by stripping away the jargon. At its core, retail accounting is simply the process of tracking every dollar that flows in and out of your store. This means recording daily sales, managing cash flow, handling payroll, and, most critically, keeping a precise handle on your inventory.

However, it goes deeper than just recording transactions. Good retail accounting involves a systematic approach to tracking inventory levels and accurately calculating your Cost of Goods Sold (COGS) or, in simpler words, the direct cost of what you sell. This specific data is what gives you a crystal-clear picture of your true profitability. It’s the difference between hoping you made money and knowing exactly if you did and where it came from.

Ultimately, this practice provides the roadmap for your entire business. It tells you which products are worth reordering, where you can afford to cut costs, and how to set prices that actually protect your margins. Without it, you’re essentially flying blind, relying on “gut feelings” rather than hard data to make critical decisions.

The Core Pillars of Retail Bookkeeping

To build a solid financial foundation, you first need to master a few key areas. These aren’t just abstract concepts; they are the daily and weekly tasks that keep your store financially healthy.

Sales Tracking and Revenue Management

Your sales data is the lifeblood of your business. It is crucial to record every transaction accurately, and this goes beyond just knowing your top line. You need to meticulously track:

Returns and Refunds: These must be recorded to adjust both your revenue and your inventory levels accurately.

Sales Tax Collection: Retailers are responsible for collecting and remitting sales tax. Your system should track this automatically to ensure compliance with local and federal regulations.

Expense Management

Retail businesses face a unique set of expenses. Rent, utilities, payroll, marketing, and the cost of the goods themselves all eat into your profits. And, if you sell on credit or extend payment terms, you also have to consider how different bad debt approaches like the direct write-off method may affect both your books and profitability.

But tracking expenses isn’t just about recording what went out the door; it’s about organizing that information in a way that reveals patterns. The real power lies in categorization. When expenses are consistently grouped and clearly labeled, they stop being scattered transactions and start becoming actionable data.

By using accounting software to separate costs into specific categories (for example, “marketing” instead of a vague “miscellaneous” bucket), you gain visibility into spending trends, margin pressure points, and areas where costs may be creeping up unnoticed. That clarity is what allows you to make proactive adjustments instead of reactive cuts.

Cash Flow Management

Managing cash flow means balancing your payables (what you owe to suppliers) with your receivables (payments from customers, though in retail this is mostly immediate sales). Negotiating longer payment terms with vendors and being cautious about overstocking inventory, which ties up capital that could be used elsewhere, is key to keeping cash flow healthy.

Believe me when I say, it’s completely possible to be profitable on paper but still go out of business if you’re mismanaging your cash flow. So, understanding how money moves through your business is crucial to its success.

Inventory is usually the largest asset on a retailer’s balance sheet. How you value it determines your COGS and, ultimately, your net income. There are several ways to approach this, and the method you choose can have significant financial implications, especially in times of inflation or price fluctuation.

Did you know?Because inventory is expected to be sold or used up within a year, it qualifies as a current asset? To learn more on this, check out Is Inventory a Current Asset? (Answered).

The Retail Inventory Method (RIM)

The retail inventory method is a popular technique, particularly in department stores and apparel retail, because it simplifies the valuation process. Instead of tracking the actual cost of each individual item, RIM uses the relationship between cost and retail price.

How It Works

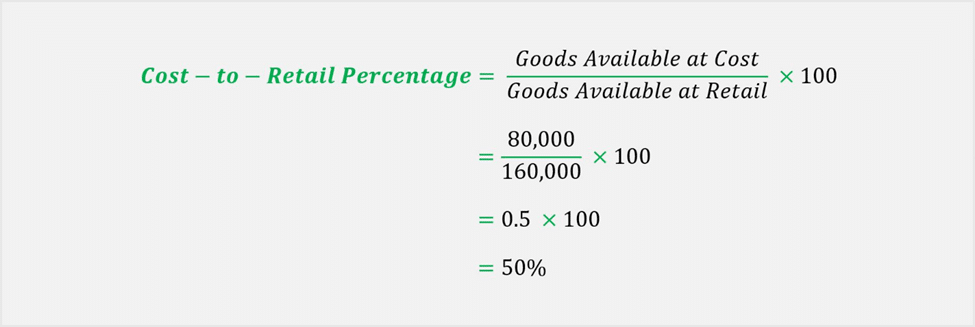

You calculate a cost-to-retail percentage (cost complement) by dividing the cost of goods available for sale by their retail value and multiplying that by 100.

Cost-to-Retail Percentage = (Goods Available at Cost / Goods Available at Retail) x 100

You then apply this percentage to your ending inventory at retail value to estimate its cost.

So, RIM is essentially an averaging technique. Instead of tracking the specific historical cost of every individual item, it uses a cost-to-retail ratio.

Here’s a working example:

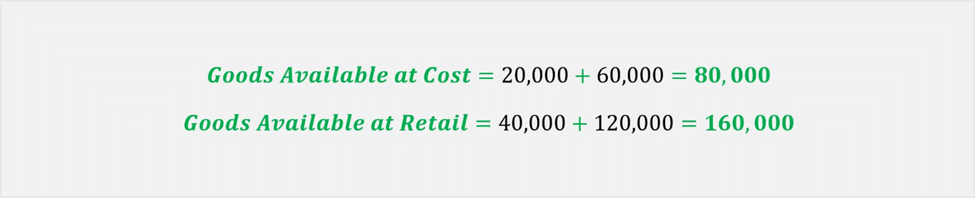

Let’s imagine you have a starting inventory that cost you$20,000 but retails for $40,000. You then purchase additional stock costing $60,000 with a retail value of $120,000. Combined, you have $80,000 worth of goodsat cost that you could sell for $160,000 at retail.

Goods Available at Cost = 20,000 + 60,000 = 80,000 Goods Available at Retail = 40,000 + 120,000 = 160,000

Applying the cost-to-retail percentage formula, this gives you a cost-to-retail ratio of 50%.

Cost-to-Retail-Percentage = (80,000 / 160,000) x 100 = 0.5 x 100 = 50%

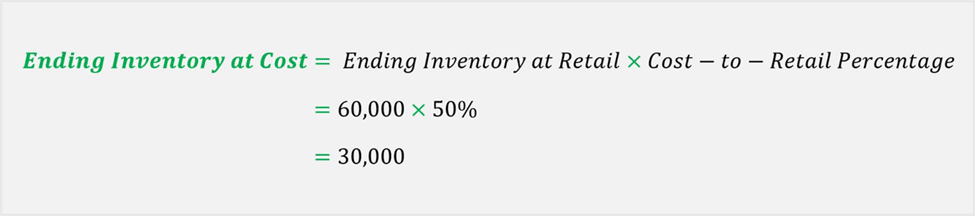

Now, suppose you generate $100,000 in salesfor the month (at retail prices). This leaves $60,000 worth of goods still on your shelvesat retail value.

Ending Inventory at Retail = Goods Available at Retail – Sales = 160,000 – 100,000 = 60,000

To determine what that inventory actually cost you (i.e., the number that belongs on your balance sheet) you simply apply your 50% ratio, arriving at an estimated ending inventory of $30,000 at cost.

Ending Inventory at Cost = Ending Inventory at Retail x Cost-to-Retail Percentage = 60,000 x 50% = 30,000

And this entire retail inventory method can be condensed into this single compact formula:

Ending Inventory at Cost = (Retail Available – Sales) x (Goods Available at Cost / Goods Available at Retail)

As you can see, this method is efficient, but it assumes a consistent markup across your entire store.

For instance, if you’re selling both high-margin service contracts and low-margin replacement filters, that 50% average can become misleading.

Pros and Cons

RIM is easier and less time-consuming than cost accounting; however, it relies on consistent markups. If you have frequent or significant markdowns, the method becomes less accurate because it doesn’t track costs at theitem level.

Cost Accounting Methods

For more precise tracking, many retailers use cost-based methods. These methods below focus on theactual cost incurred to acquire the inventory.

FIFO (First In, First Out): This method assumes that the oldest inventory (the first in) is sold first. During inflation, FIFO results in a lower COGS and higher net income because you’re selling the older, cheaper stock first.

LIFO (Last In, First Out): LIFO assumes the newest inventory is sold first. This matches current costs with current revenues but is less common internationally. During inflation, it leads to a higher COGS and lower taxable income.

Weighted Average Cost: This smooths out price fluctuations by averaging the cost of all similar items in stock. It’s a good middle ground for businesses with large volumes of identical goods.

So, Which One Is Better?

Which method is best will depend on your business model.

A small boutique with stable prices might prefer the simplicity of RIM. While a business dealing with volatile costs or high-value items might need the accuracy of a specific identification or FIFO method.

Experts note that while RIM is a century-old standard, cost accounting is often better equipped to integrate with modern digital tools and provides more accurate, item-level visibility.

💡 Pro Tip: Beyond just valuing your inventory, track your “inventory turnover rate” by product category. This metric tells you how many times you’re selling through your stock in a given period. Pairing this with your chosen valuation method reveals which items are actually earning their keep on the shelf versus which ones are tying up cash that could be deployed elsewhere.

Under RIM, when the cost of importing goods changed due to tariffs, the cost-to-retail ratio shifted dramatically. This caused “wild swings in margin estimates,” forcing them to pull their profit guidance. Why? Because RIM revalued all inventory based on the new ratio, including old stock not subject to the tariffs.

A cost accounting method would have only applied the new costs to the specific items purchased under the new tariff regime, providing a much clearer picture. It highlights a crucial point: sometimes, accuracy is worth the extra effort.

Financial Statements for Retailers

Now, all of this data collection and tracking leads to the creation of threeessential financial statements. These reports tell the story of your business.

The Balance Sheet

Balance sheets answer the question: What do I own, and what do I owe?

This is a snapshot of your business’s financial position at a specific moment. It lists your assets (cash, inventory, equipment), your liabilities (loans, accounts payable), and your owner’s equity. It answers the question: What do I own, and what do I owe?

The Income Statement (Profit & Loss)

Income statements answer the question: Did I make a profit?

This statement shows your performance over a period of time (e.g., a month, a quarter, a year). It starts with your revenue, subtracts the cost of goods sold to find your gross profit, and then subtracts your operating expenses to reveal your net income. It answers the question: Did I make a profit?

The Cash Flow Statement

Cash flow statements answer the question: Do I have enough cash to pay my bills right now?

This tracks the actual movement of cash in and out of your business. It breaks cash flow into operations (sales and expenses), investing (buying equipment), and financing (loans). It answers the critical question: Do I have enough cash to pay my bills right now?

💡 Pro Tip: Use your historical income statements to build a rolling 13-week cash flow forecast. While your balance sheet and P&L tell you where you’ve been, a short-term forecast forces you to anticipate slow sales periods or large vendor payments before they hit your bank account, giving you a crucial window to adjust spending or secure financing.

Best Practices for Retail Bookkeeping

Implementing strong habits is the only way to ensure your financial data remains reliable.

Effective retail bookkeeping comes down to consistency, separation, and smart systems. The following practices focus on daily discipline, clear financial boundaries, and the use of tools that reduce errors and save time. When these fundamentals are in place, your financial records stay accurate and actionable.

1. Establish Daily Routines

Don’t let transactions pile up. Reconcile your sales records from your POS system with your bank deposits daily. This helps catch errors or discrepancies immediately rather than a month later when it’s nearly impossible to trace them.

2. Separate Business and Personal Finances

Now, this is a non-negotiable for success. Mixing personal and business transactions creates a confusing mess that makes tax preparation a nightmare and obscures the true performance of your store. Always use a dedicated business account.

3. Leverage Technology

Manual bookkeeping in spreadsheets is risky and time-consuming. Modern accounting software can integrate directly with your POS system and bank accounts. This automation handles the heavy lifting from categorizing expenses to reconciling transactions, and generating reports, freeing you up to focus on your customers.

The Power of Integration

I once consulted for an electrical supply house that was using a generic spreadsheet for inventory and a separate system for sales. They were spending three days every month manually matching sales receipts to inventory counts.

By implementing integrated inventory software, we cut that down to a few hours. More importantly, the owner could finally see, in real time, that a particular line of high-end lighting fixtures wasn’t turning over as fast as he thought.

He was then able to run a targeted promotion and clear the stock before it became a cash-flow anchor. That is the power of modern retail accounting.

💡 Pro Tip: Even with the best software, be sure to schedule a fixed time each week for financial review. I personally live by this rule and use that dedicated time to pay bills, review outstanding invoices, and check cash flow forecasts. This consistency prevents bookkeeping from becoming a once-a-year scramble.

Taking the Helm of Your Business

Retail accounting is far more than a compliance exercise or a set of tedious bookkeeping tasks. It is the diagnostic tool for your business’s health, the objective narrator of your business’s story.

As we’ve explored, whether you’re a solo entrepreneur or a multi-branch operation, the choices you make, from how you value inventory to how diligently you track your cash flow, directly determine your ability to navigate challenges, seize opportunities, and build a lasting enterprise.

The path to mastering your finances doesn’t require you to become a CPA overnight. It simply requires a commitment to moving from guesswork to knowledge. This means choosing the right systems, whether you prioritize the speed of the retail inventory method or the precision of cost accounting. It means establishing the daily discipline to let your numbers guide you, not surprise you.

Don’t get so lost in the day-to-day grind of ringing up sales that you ignore the powerful narrative your financial data is trying to tell you. That narrative holds the answers to your most critical questions: which products deserve more shelf space, where your margins are truly leaking, and when you have the financial freedom to take that next big risk.

So, start listening today. By taking control of your numbers, you can stop flying blind and finally take the helm of your business’s future.

FAQs

1. How often should I physically count my inventory if I’m using the Retail Inventory Method?

Even if you use RIM for internal reporting, you should still perform a physical inventory count at least once or twice per year to verify accuracy and adjust for theft, damage, or supplier errors that your estimates might miss.

2. What is the difference between gross margin and markup, and why does it matter?

Markup is what you add to the cost of a product to set a selling price, while gross margin is the percentage of revenue you actually keep after that product sells; confusing the two is one of the fastest ways to accidentally underprice your goods.

3. Do I need to use a different accounting method if I sell both products and services?

Yes, many hybrid businesses benefit from using project or job costing for their services while maintaining the retail inventory method for products, as this separation provides clearer insight into which side of your business is truly driving profits.

4. Can I switch my inventory valuation method from RIM to FIFO down the road?

You can switch, but it requires approval from the IRS (using Form 3115) and comes with administrative complexity, so it’s wise to choose the method that best fits your long-term strategy rather than planning to change later.

5. What is “shrinkage” and how should I account for it?

Shrinkage is the loss of inventory due to theft, error, or damage; you should account for it by recording a periodic adjusting entry that increases your Cost of Goods Sold and decreases your inventory asset to reflect what’s actually on your shelves.

Share:

Facebook

Twitter

Pinterest

LinkedIn

James R. Leichter

James R. Leichter, renowned HVAC business consultant, author, and public speaker, is dedicated to empowering HVAC businesses with innovative strategies and insights. Leichter, affectionately known as 'Mr. HVAC,' brings over 27 years of industry expertise and a passion for practical solutions, assisting HVAC businesses to streamline operations and maximize profits. Discover transformative guidance at MrHVAC.com.

Quick Answer The purchase order (PO) process is the step-by-step workflow businesses use to control purchasing, approve spending, document vendor agreements, verify deliveries, and pay