Cost accounting is simply the practice of tracking, analyzing, and controlling the costs associated with running your business. The cost visibility that this type of accounting provides helps you ensure your financial decisions are grounded in reality.

Understanding the true cost of your product or service is the secret to profitability, yet many small business owners rely on gut feeling rather than hard data.

Most business owners I meet through Aptora and my consulting work are fantastic at their craft. They know how to diagnose a tricky electrical fault or size a commercial boiler in their sleep. But, when it comes to understanding where their profit actually comes from, the lights start to dim.

The sad reality is, most business owners never get this level of visibility into their costs, and as a result, they leave profit on the table without even realizing it. Cost accounting changes that. It gives you a clear, structured way to understand how your business truly performs which is essential your business’s success.

So, now that we’ve established its importance, what exactly does cost accounting involve, and what methods and tools can you employ to successfully run your business? Let’s explore.

Key Takeaways

Clear Cost Visibility: Cost accounting shows the true cost of each product or service, enabling better financial decisions.

Direct and Indirect Costs Matter: Understanding fixed, variable, direct, and overhead costs prevents underpricing and missed profits.

Method Selection Drives Accuracy: Job costing, process costing, or activity-based costing should match your business model for precise insights.

Contribution Margin Guides Decisions: Calculating the contribution margin helps evaluate special orders and short-term pricing strategies.

Software Simplifies Complexity: Tools like Aptora 360 automate cost tracking, reduce errors, and provide real-time insights for better business management.

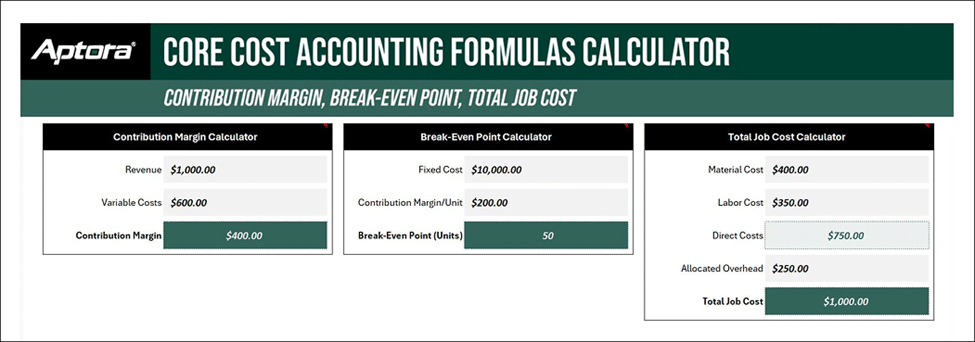

📥 Stop guessing your numbers and start calculating them!

Download our FREE Core Cost Accounting Formulas Calculator to quickly calculate your Contribution Margin, Break-Even Point, and Total Job Cost in seconds, so you can make smarter pricing decisions backed by real numbers, not assumptions.

Deeper Dive: What is Cost Accounting and Why Should You Care?

Again, at its core, cost accounting is the methodology of recording, classifying, and allocating all the expenses associated with your processes, projects, or products.

Think of it as a high-powered microscope for your finances. While your standard bookkeeping (or financial accounting) tells you if your business made a profit overall last month, cost accounting tells you which specific jobs or products actually made you money and which ones lost it.

Think about your own business for a moment. You know what you pay for materials, easy. You know what you pay your technicians, a no-brainer. But, do you know what that service call actually costs when you factor in the truck maintenance, the dispatch coordinator’s salary, the liability insurance, and the twenty other tiny expenses that sneak into every job?

For an amateur owner, this insight is gold. It moves you from simply tracking transactions to actively managing your business’s efficiency and, in addition to the ones above, answering critical questions like:

Should I accept that large special order at a discounted rate?

Am I pricing my services correctly?

Where can I cut costs without sacrificing quality?

Breaking Down the Building Blocks: Types of Costs

Before we dive into the methods of cost accounting, you first need to understand some of the basic language of accounting and, most importantly, cost. Every expense in your business will fall into one of four key categories: fixed costs, variable costs, direct costs, and indirect costs.

Fixed vs. Variable Costs

Fixed Costs: These are the expenses that stay relatively the same no matter how much you produce or sell. Think rent, insurance, salaried employee wages, and software subscriptions. They are the baseline cost of keeping your doors open.

Variable Costs: These costs fluctuate directly with your production volume. If you produce more, they go up; if you produce less, they go down. Common examples are raw materials, direct labor (hourly wages), and shipping costs.

Direct vs. Indirect Costs

Direct Costs: These can be traced directly and easily to a specific cost object, like a product, service, or project. For a construction company, the lumber for a specific deck and the wages of the crew building it are direct costs.

Indirect Costs (Overhead): These are costs necessary for operations but not directly tied to a single product. Examples include the salary of a project manager overseeing multiple sites, general office supplies, and utilities for the headquarters.

💡 Pro Tip: A simple way to distinguish direct from indirect costs is to ask: “If we stopped working on this one specific project today, would this cost disappear?” If the answer is yes (like materials for that job), it’s likely a direct cost. If the cost remains (like the rent on your office), it’s an indirect cost or overhead.

How to Allocate Overhead (Without Guessing)

While we’re on the topic of direct vs indirect costs, I want to break away and quickly cover one of the hardest parts of cost accounting, which is assigning indirect costs fairly and consistently. A simple and effective way to do this is with an overhead rate. Here’s the basic overhead rate formula:

Basic Overhead Rate Formula

Overhead Rate = Total Indirect Costs / Total Allocation Base

Common allocation bases include:

Labor hours

Machine hours

Revenue per job

Let’s see it in practice with this working example:

If your monthly overhead is $20,000 and your team works 2,000labor hours, your overhead rate will equal $10 per labor hour.

$10 per labor hour = $20,000 / 2,000 hrs.

So, if a job takes 10 hours, you assign $100 of overhead to that job.

❗ Without a consistent method for assigning overhead costs to each job, those expenses are often overlooked or spread unevenly, which leads directly to underpricing.

How Cost Accounting Differs from Financial Accounting

There are many types of accounting for business, and before we examine cost accounting methods, let’s clarify the difference between financial accounting and cost accounting, two terms that are often conflated.

I often use this driving analogy when I speak at conferences: Financial accounting is like looking in your rearview mirror. It shows you where you have been, and it is essential for keeping you legal and out of trouble with the authorities. Cost accounting on the other hand is your windshield. It shows you the road ahead.

Financial accounting also follows strict rules. Generally Accepted Accounting Principles (GAAP), dictate how you must report your numbers to the outside world. It is necessary. Your bank wants to see it. The IRS demands it. But, those rules were not designed to help you run your business better.

Cost accounting plays by a different set of rules entirely. It asks questions like: What if we changed our pricing structure? What if we stopped offering a particular service? What if we invested in new equipment? These are the questions that determine whether you will still be in business five years from now.

Exploring the Different Cost Accounting Methods

Now, let’s jump into cost accounting methods. Over the years, I have seen every variation of costing methodology you can imagine. Some work beautifully for certain businesses. Others create more confusion than clarity. Let me walk you through the approaches that I know actually deliver results.

Job Costing vs. Process Costing

Job Order Costing: This method is used when your products or services are unique or easily distinguishable. It tracks costs for each individual “job.” This is perfect for construction companies, custom manufacturers, marketing agencies, and law firms. You essentially build a cost sheet for every project.

Process Costing: If your business produces identical, homogenous products in a continuous stream, process costing is your friend. It averages the total costs over all units produced. Think of industries like food processing, oil refining, or chemical manufacturing.

Again, neither approach is inherently superior. The right choice depends entirely on how your business operates.

Activity-Based Costing (ABC)

If you have a complex business with diverse products and high overhead, activity-based costing (ABC) offers the most accurate picture.

Instead of simply lumping overhead costs together and spreading them around, ABC identifies all the different activities that go into production (like machine setups, quality inspections, and purchase orders) and assigns costs based on how much of each activity a product actually uses.

For example, a simple product might require one setup, while a complex one requires ten. ABC would assign ten times the setup cost to the complex product, revealing its true cost. This is invaluable for pricing and identifying inefficiencies.

Core Cost Accounting Formulas

Next, to truly understand your costs, you need to have a few foundational formulas down pact. These are not complicated, but they are powerful.

Contribution Margin (Your Profit Engine)

Contribution Margin = Revenue – Variable Costs

This formula tells you how much money is left to pay for fixed expenses and generate profit after covering variable costs.

Example: If a job brings in $1,000 and variable costs are $600, your contribution margin is $400. That $400 goes toward overhead and profit.

Break-Even Point (When You Stop Losing Money)

Break-Even Point (Units) = Fixed Cost / Contribution Margin per Unit

This formula shows how much you need to sell to cover your costs.

Example: If your fixed costs are $10,000/month and you make $200 contribution margin per job; you need 50 jobs just to break even. Total Job Cost (Your True Price Floor)

Total Job Cost = Direct Costs + Allocated Overhead

This tells you the true cost of completing a job with direct costs and overheadincluded, and the minimum amount you must charge to avoid losing money on a job.

Example:

If direct materials cost $400, direct labor is $350, and allocated overhead is $250, your total job cost is $1,000.

How Cost Accounting Looks in Your Books (Simple Journal Entries)

Cost accounting doesn’t just live in reports; it shows up directly in your books. As each job progresses, costs are recorded, assigned, and eventually recognized as expenses. The entries below show how that process works behind the scenes:

Journal Entry Example 1: Recording Materials for a Job

Account | Debit ($) | Credit ($) ----------------------------|-----------|------------ Work in Progress (WIP) | 250 | Materials Inventory | | 250

This assigns labor directly to the job being performed.

Journal Entry Example 3: Applying Overhead

Account | Debit ($) | Credit ($) ----------------------------|-----------|------------ Work in Progress (WIP) | 150 | Overhead Applied | | 150

This is how indirect costs get assigned to jobs using your overhead rate.

Journal Entry Example 4: Completing the Job

Account | Debit ($) | Credit ($) ----------------------------|-----------|------------ Cost of Goods Sold (COGS) | 700 | Work in Progress (WIP) | | 700

This moves the total cost of the job into your expenses once it’s finished.

💡 Pro Tip: While you’ll likely employ a software that handles this automatically, take time to understand how it works. These journal entries are what powers accurate job costing behind the scenes.

Marginal Costing for Short-Term Decisions

Also known as variable costing, marginal costing focuses only on the variable costs of production.

This is incredibly useful for making short-term decisions, like pricing a one-time special order. It helps you calculate the contribution margin (i.e., the amount left over from sales revenue after variable costs are covered) which then goes toward paying your fixed costs and generating profit.

💡 Pro Tip: When considering a discount for a large order, use marginal costing. As long as the price covers all yourvariable costs (materials, labor, etc.) and still leaves a positive contribution margin towards your overhead, the order can be profitable (even if it seems low compared to your usual price).

A Quick Decision Framework for Pricing

When a special order or discount opportunity comes up, you often don’t have time for deep spreadsheet analysis. This simple framework can help you quickly decide if the deal is worth taking.

Step 1: Identify Your Minimum Acceptable Price

Your minimum price should at least cover your variable costs per unit:

Why it matters:

If the offered price is higher than your variable cost, you’re covering production costs and contributing to fixed costs and profit.

If it’s lower, taking the order would increase losses.

Step 2: Calculate the Contribution

Contribution per unit = Offered Price – Variable Cost

Example:

Variable cost = $75

Offered price = $90

Contribution = $15

Even if your regular selling price is $150, accepting this order may make sense as a short-term strategy because it still adds profit to cover fixed costs.

⚠️ Important Note: This approach only works if you have unused capacity. If your production is already at full capacity, discounting could reduce overall profitability by displacing higher-paying orders.

The Pitfalls of Spreadsheets: Why DIY Costing Fails

Many business owners start by using spreadsheets to track expenses and profits. That works fine when operations are small, but as the business grows, spreadsheets quickly become cumbersome, error-prone, and frustrating. It’s no wonder so many small business owners struggle to see the full picture of their true costs.

Spreadsheets create three major challenges:

Human Error: A single mistyped formula or a transposed number can ruin a project’s profitability.

Time Drain: The hours you spend hunting for numbers and updating sheets are hours you’re not spending on strategy or sales.

Lack of Real-Time Data: By the time your spreadsheet is updated, the data is often old. You need real-time insights to stop a budget overrun before it happens, not three weeks later when you reconcile the books.

Implementing a proper cost accounting system can help with this, though it also relies on accurate data entry to avoid mistakes and requires careful setup. This is where dedicated software becomes essential.

Tools like Aptora 360 can automate calculations, integrate all your data in real time, and make accurate job costing immediate and effortless. Learn more about Aptora 360.

The Path Forward

So, whether you run a construction company, a marketing agency, or a manufacturing plant, the principles remain the same. Cost accounting gives you x-ray vision into your own business. It reveals the hidden profits and exposes the invisible losses.

Understanding that, the question then now is not whether you can afford to implement better cost accounting. The question is whether you can afford not to.

After twenty-seven years in this industry, I can tell you with absolute certainty: the businesses that thrive over the long term are not necessarily the ones with the highest revenue or the flashiest marketing. They are the ones that truly understand their numbers. They are the ones that know, with confidence and clarity, exactly where their profit comes from.

Strive to be one of “the ones.”

FAQs

1. How often should I review my cost accounting data?

At a minimum, review it monthly, but weekly reviews are ideal for catching issues early. High-volume or fast-growing businesses may benefit from real-time tracking.

2. What’s the biggest mistake small businesses make when starting cost accounting?

They underestimate indirect costs and overhead, which leads to underpricing. Even small overlooked expenses can significantly impact profitability over time.

3. Do I need an accountant to implement cost accounting?

Not necessarily, but professional guidance can help you set it up correctly from the start. Many modern software tools simplify the process enough for owners to manage it themselves.

4. How long does it take to see results from cost accounting?

You can start gaining insights within weeks, especially around pricing and job profitability. More meaningful trends and optimization opportunities typically emerge over a few months.

5. Can cost accounting help me grow my business, or just control costs?

It does both by revealing which products, services, or customers are most profitable. This allows you to double down on what works and scale more strategically.

Share:

Facebook

Twitter

Pinterest

LinkedIn

James R. Leichter

James R. Leichter, renowned HVAC business consultant, author, and public speaker, is dedicated to empowering HVAC businesses with innovative strategies and insights. Leichter, affectionately known as 'Mr. HVAC,' brings over 27 years of industry expertise and a passion for practical solutions, assisting HVAC businesses to streamline operations and maximize profits. Discover transformative guidance at MrHVAC.com.

Quick Answer The purchase order (PO) process is the step-by-step workflow businesses use to control purchasing, approve spending, document vendor agreements, verify deliveries, and pay